65 used to be retirement age (for men at least), it clearly needed raising years ago, but was hard to do politically in many countries. It is finally being raised. When pensions were first introduced they were meant to run 5 years, not 20.

In the UK, at least, you could argue we're left paying for a generation of Baby Boomers who are swanning about on cruises, golf days and health spas on pensions they never paid even half towards.

Most are perfectly able to work for another 10 years at least (and if you're younger than 50 you'll have to work those extra 10 years), but for some reason we need economic migrants for economic growth. Even though we're not building anywhere near enough homes, schools, hospitals and transport infrastructure for this mass immigration, and we're not training enough nurses, doctors, teachers. We are effectively just shunting all the economic problems of the end of continual growth 20 years down the line. We even scrapped bursaries for student nurses! Utter madness.

And then, rather ironically, it's this same generation who overwhelmingly voted for Brexit to even further destroy their children's and their children's children prospects because they're not happy about the changing face of the Britain they're not even going to live in.

> in the UK, at least, you could argue we're left paying for a generation of Baby Boomers who are swanning about on cruises, golf days and health spas on pensions they never paid even half towards.

There is a massive (and sadly too common) social bias in this comment: this is not the life of retired baby boomers, this is the life of retired upper-class baby boomers, but the majority of people isn't like that.

The upper class people also live a lot longer than the lower one (a decade or more depending on the region) so they cost even more.

And since they are generally in a much better shape at the same age, raising the retirement age affects the lower class much more than the upper one.

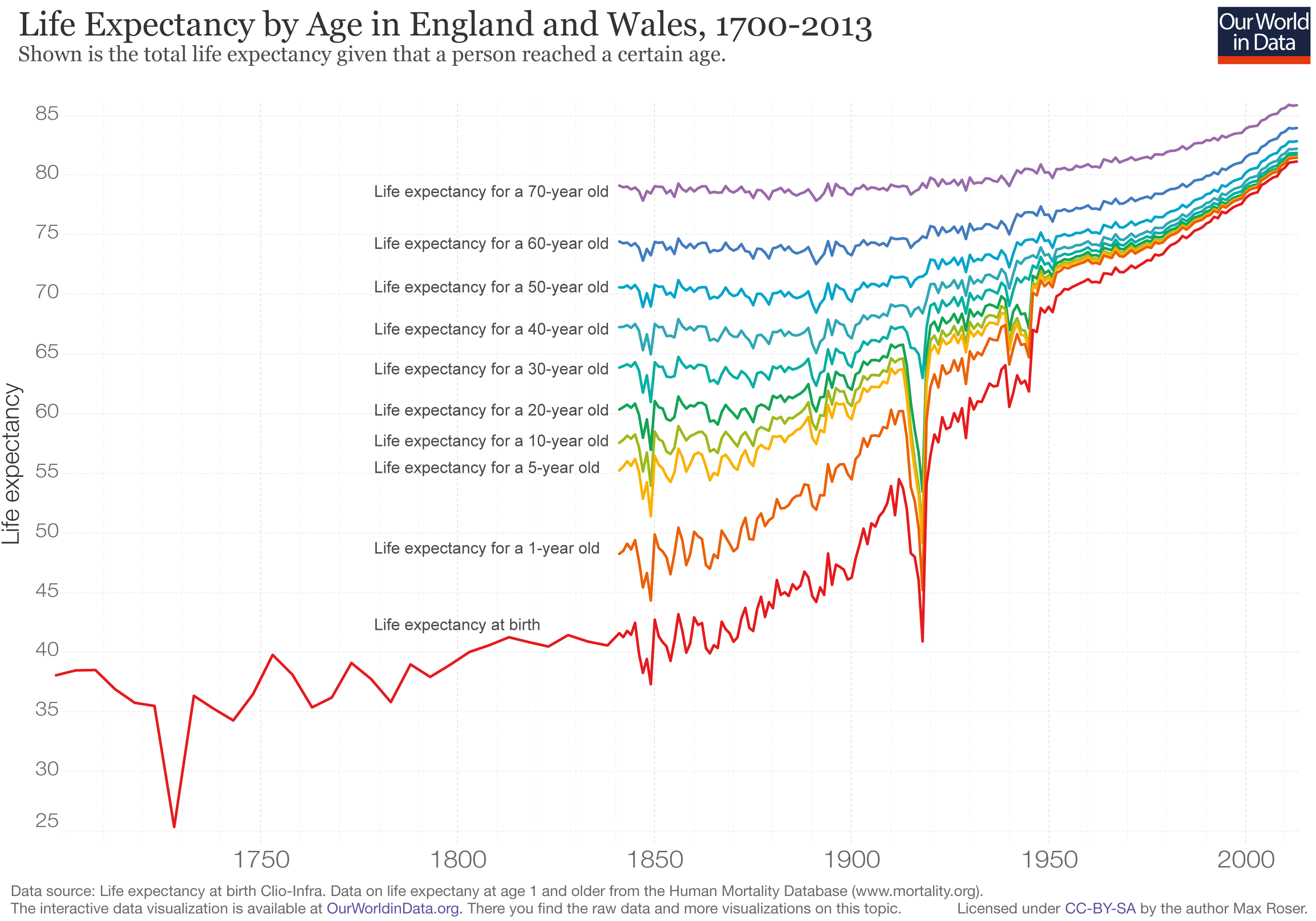

Also, the life expectancy didn't change as dramatically as you'd think since 1950 in that context: in 1950 the life expectancy of a 60 years old British citizens was 77 years. Now it's around 84 years[1]. It rose, but not that much (it didn't go from 5 to 20).

The middle class is where all those cruises are being sold to.

They have huge disposable incomes due to final salary pensions and no mortgage to pay, or they've downsized and unlocked huge sums in an over-inflated housing market because we stopped building enough homes year on year 40 years ago when Thatcher banned the councils from doing so.

Pensioners now have higher disposable incomes on average than working people in the UK.

The average person under the age of 50 today will never have it as good as the baby boomers, unless some major, socially liberating, tech advance happens.

This is indeed correct. But a 60% increase isn't a 400% one, and talking about the increase of healthcare cost is very different from complaining about «lazy and selfish babyboomers going to the spa instead of working longer».

These are the two things I criticized in the original comment.

> 65 used to be retirement age (for men at least), it clearly needed raising years ago, but was hard to do politically in many countries. It is finally being raised. When pensions were first introduced they were meant to run 5 years, not 20.

Working beyond 65 is fine for some people but there are many cases where this isn't. Take any job requiring physical labour like construction. There is only so long you can do those kinds of jobs. Also the fact that you've been doing them for decades takes its toll, physically.

So what's the solution there? People still need stuff built. So you only work construction until you're 40-50 and then what? Change careers? To what exactly?

Even for jobs that aren't physically demanding, many people have jobs that if they lose them when they're over 50 they may never work again. This could be completely not their fault either. Their company could go under or get bought out. It could be economic downsizing.

The problem, on HN at least, is that there are young people in a high-demand high-paying profession who have never experienced a recession making sweeping statements like "just work until you're 70" as if everyone else is in the same boat as them.

As much as you might be a highly paid tech worker, come back here when you're say 55 and those same companies who were fawning over you as a new college grad won't give you the time of day. In tech we haven't really dealt with this yet but I guarantee you it's coming.

I don't like generalizing by "generations" but this is something where I see a divergence in younger and older coworkers.

Older ones literally say, "I don't want to learn [insert relevant skill] because I'm too old."

Younger coworkers seem to come better equipped with the mindset that they will have to continually unlearn and relearn to remain relevant. And to counter your point about a recession, many of them started their careers in a recession and I see it in their conservative approach to employment.

I think this is more about a complacent mindset with people who may not have recognize that they have to adjust to continue to be valuable. I've known people who were downsized and squandered ample opportunity like free tuition to change careers. I've known others who've successfully parlayed a physically demanding job to one less physically demanding because they knew they couldn't do that forever.

What company, exactly, is going to want to invest time and money training a man in his late 60s to do a job that will afford him a reasonable lifestyle in a large metropolitan area?

I think you are assuming there are no transferable skills and the person would have to trained from square 1. As an example of where this isn't the case, I know an older lineman who recently moved into a design slot. Sure, he needed some training but he also brought a wealth of other value, like design for maintainability

>65 used to be retirement age (for men at least), it clearly needed raising years ago

How old are you? Have you tried working at most jobs (not just some office job) as 65+? Have you tried programming as such?

If you mean "paying pensions for people 65+" was too much, and we needed to cut that, I'd understand. And sure, raising the retirement age is one way to do that.

Still, it's not the best way to solve the problem. Nor is it "needed" for any other reason (e.g. because people of 65+ today are more capable than in the 70s).

>Most are perfectly able to work for another 10 years at least

You can't pay for someone to not work for 20 years; who's going to pay?

There isn't enough wealth to cover it. All the wealth of all the billionaires in the world is only the EU healthcare budget for five years.

Productivity is what generates wealth, and we can't afford to have a large class of people merely consumptive. People aren't producing enough to do it.

If you want to give 20k/yr to someone it has to come from someone else. That's putting younger generations into a dire financial position.

Work of some form has to be found, even if it isn't covering living expenses for pension-age people. Some form of off-setting the cost has to be implemented, or else there'll be a political and economic crisis.

Since 1950 the retirement duration only grew by 50% (the life expectancy at 60 went from 77 years to 84 [1]) can you recall how much the productivity grew from that time ? If we cannot afford to pay 50% more when productivity grew by a factor 3[2], there is indeed a problem of repartition.

The relevant growth % is the total number of life-years being funded by retirement.

Since the total populaton of US in 1950 was 150, and is 300 million today -- assuming equal distribution of ages -- that's a 4x increase in life-years to fund.

ie., 2x for population size, and 2x for length of retirement

And worse, the distribution isnt equal, ie., there are more of the population today in retirement than in 1950.

So it's at least 4x the number of years, and probably closer to 6x.

No need to take the population into account because I used the per capita productivity.

And do you have figures for the doubling of the retirement duration ? As I showed above, it only increased by 50% in England and I'd be surprised is the American raise was higher since life expectancy is lower there (in part due to a less efficient health system).

Well it's a rather difficult calculation to make in this fashion.

The relevant data needed is total number of retirement hours funded, total productive output, and total "other" essential spending.

What's also happening is the cost of healthcare is increasing, quite dramatically, and eating up productivity gains.

I have a strong suspicion that we're way ahead of "general essential" social spending today, compared to 1950s, per-captia; productivity gains included.

>You can't pay for someone to not work for 20 years; who's going to pay?

For one, people pay pension savings throughout their careers (in most civilized countries).

Second, we've already discussing UBI for life, compared to which "paying people not to work for 20 years" is nothing.

Third, money to pay people is an artificial construct, which is not really what's missing. We have the wealth to sustain them. E.g. we have increased productivity dozens of times over the past 100 years, and yet we don't enjoy those fruits in increased leisure time or work-less access to food, health, studies, shelter, etc. If anything the latter have inflated many times over. Where are those "trickle down economics"?

>Productivity is what generates wealth, and we can't afford to have a large class of people merely consumptive.

We have increased the productivity of the average worker dozens of times over the past 100 years. How's that wealth distributed?

The idea is that your future pension is paid by yourself gradually over your productive years. Generally speaking of course - some have no work ever, some do and pay more, some die before they get some of it, and so on.

Complex calculations though, since we can't know the situation 40 years ahead, perhaps not even 5 years ahead.

This is the thing I don't get. Do you not understand that it's not sustainable? That this generation will quite probably be the only one to ever get away with it? That the following people who are 20 now will not have these luxuries when they are 65?

The sad fact is that expecting to be in a high-flying job your entire career and to only climb is no longer viable. Yes, older people will have to take lesser jobs, but that's what we're all going to have to do.

We can't afford to pay for people to have a second childhood when they can still do lots and lots of jobs.

It is also worth remembering that today's 65 year olds are nowhere near as run down as those 50 years ago. We've got better diets, better medicine, generally less demanding jobs, etc.

And I'm 40 and my 78 year old father only really started detiorating noticeably 3 or 4 years ago and would still be capable of many, many jobs.

I appreciate some older people won't be able to, but it's only fair that being unfit for work due to infirmity should be assessed as any other disability and paid for like any other welfare.

I’d argue it’s working every healthy day of your life is what’s not sustainable. You shouldn’t be paying people to do anything. People can earn their retirement, whether it’s through pension, social security, or personally funded IRA/401k or a reverse mortgage on property accumulated and paid for over the previous decades.

45 years of work should be more than enough economic output for one person to be able to get a “second childhood” as you call it. What the heck are they working for in the first place?

Speaking from Finnish perspective here. The thing is that the boomer generation did not save their pensions. We have a system where future generations pay.

It worked ok back when population grew. Now it doesnt. Basically they voted that their kids will pay for their pensions and then didnt have enough kids. So now we are quite screwed.

> 45 years of work should be more than enough economic output for one person to be able to get a “second childhood” as you call it. What the heck are they working for in the first place?

By simple approximation, assuming a real rate of return between 2% and 6%, you need to consistently save and invest 10% to 30% your working life income consistently for 45 years to fully fund about 20 years of non-work / retirement. The whole point of the pension problem is that most people are not able or willing to do that.

You've seen the charts, right, showing productivity vs wages since the 80s? We enjoyed a second era of industrialization, with huge advances in efficiency and productivity, and again the benefits were all captured by those at the top.

If society had been structured for the last 4 decades like it had been the previous two, we'd be talking about lowering the retirement age.

I'm in my mid-40s and I'm already burned out on work. I am desperate to retire. I can't imagine working past retirement age, just because I am still capable to do so.

Ditto, but despite having mortgage paid off and healthy 401k, I have 2x kids college expenses coming up over the next 12 years. I’m resigned to working till I drop dead. 63, or whatever Medicaid will be at, is the minimum.

As a college student, you really aren't doing your kids any favors by paying for their college. Its not going to teach them the value of money when they have never earned anything themselves and their tuition is magically paid.

Taking loans and working in the summer/internships to pay it off, without being reliant upon your parents is the ideal to aim for.

After all, I think Warren Buffet said that he plans to give enough to his children so that they could anything, but not enough so that they can do nothing.

As someone who paid his own way through college, I disagree entirely. There's nothing heroic about taking out loans. Not having to worry about college expenses allows one to focus on college and all the benefits that college has to offer. I never got to take an internship. Wanna know why? Because I had to ensure that I had enough money for the next semester, and I wasn't going to go from making $10 an hour back to $4.25 just so that I could go be an underling... I couldn't have afforded the next semester.

Buffet is giving his kids retirement money, not yacht money. They've all been in the work force for decades.

He's still giving them far more than the price of a college education.

I guess I am really biased, being in Tech. Internships pay around half of what full times make, which as a college student is an insane amount of money. It's more than enough to graduate debt free.

I can cash flow it as long as they go in-state, then use the saved cash to buy a cheap house instead of paying for rent. No way I’d have them take out a loan if I can pay for it; just debt slavery.

Even if we used double of his everything it wouldn't be nearly enough. If you are into taking stuff away from other people for your own benefit, I suggest invading/conquering other countries.

Mean income for retirees aged is $103,000 and below [3]

So, the amount of money spent on a single largely meaningless war that the US is solely responsible for could easily increase the quality of life of quite a few people for quite a few years (if you don't dole out $140,000 in its entirety but spread in smaller chunks over the years or invest in infrastructure, medical care etc.)

Oh, if you meant to save the money spend over about two decades and use that instead to pay out retirement for one to two years, then sure. However, retirement lasts more than one to two years. One or two decades are more likely.

>This is the thing I don't get. Do you not understand that it's not sustainable?

There's nothing about it that it's not "sustainable". Pensions aren't and shouldn't be a pyramid scheme (of younger vs older generations etc).

Let's consider UBI.

A UBI of $1000/month for 300M Americans comes about $3.5 trillion/year. That's around 18% of the US GDP.

And that's flat out giving the money.

Now reduce that by the current welfare spending which is $1.2 trillion (and which you could replace with the UBI, or perhaps just keep the 0.2 trillion of it for special cases), and you get to $2.5 trillion/year, or ~13% of the GDP.

For comparison overall government spending was 38% of GDP in 2017.

Of course "free pension" would be far less than that amount, because this UBI amount is calculated for 300M people. Whereas pensioners will be only people > 65 y.o or so -- a much smaller number.

We're getting to something like 5% of the GDP or less.

And that's assuming everybody is equally entitled to that money. Which people already having wealth need not be, living even less people entitled to that "free pension" -- if you have a million in savings you don't really need that $1000/month, do you?

And of course, workers pay (or can be made to pay, with an automatic tax of say 10% month, as most civilized western countries have) for their pensions throughout their careers. So a large amount of pensions can come from that.

Not to mention the pension money wont magically disappear -- it'll be reintroduced into the economy (and further taxed etc).

With sane housing laws and no crazy lifestyles, people can live just fine on $1000/month. In fact they do just that, even with less, all over the world, including in places with more expensive food and consumer products than the USA.

The two things that need to be kept low are rent (which should be: the US has ample space to built on --nobody said pensioners have to live in Miami or NY, and should not be costing more than a few tens of thousands for the kind of constructions that pass for homes there) and healthcare (which in the US is laughably overpaid for what it offers -- I have been asked to pay $200 for perfectly common and safe procedures one can do themselves, and which in other western countries you can have at your average pharmacy for $10).

This generation is likely the only one to have a pleasant retirement because our world is headed for 3 degrees and more of warming. It's unlikely that social security systems will survive the mass migration of climate refugees.

My 38 year old friend installs security systems in homes and businesses. This job involves crawling around attics in 100+ degree heat. Trying to imagine my very healthy 60 year old father doing this is... Well it's not happening. I suspect my friend's body will be shot by 50.

Friend of mine is a builder, mid-40's and had to give it up as his back literally an S. He's doing music now, not making much atm, but least he is active and not giving up on himself as many do alas.

Then you have professional footballers - don't see any old ones doing that.

So yes, some trades/professions do take a toll and in effect have age/fitness limits that do not correspond to retirement age.

Alas, nobody tells you at school the work-expectancy cut-off age for many a profession. Hence many will do a trade, that they will be unable to do in later life and not everybody wants to or is able to be a manager or business owner.

But many people fail to plan their pensions, let alone their working/income planning for a lifetime.

FWIW many (and I'll agree) would say 35 is when you start to really notice your age catching up with your body and downhill from their.

Agreed, except for the professional footballer comment, if you can't save for retirement while making more money in a year than most people make in 10, that's on you.

Agreed, the remuneration in professional sports tends to more than compensate an early end of a career. Was an example of how a career is not limited by some arbitrary pension age but the physical impact of that career and ageing.

Alas not all career paths afford remuneration to accommodate the aspect of age limitations and the impact of that career upon health.

A lot of this could be addressed by employers being more comfortable with part-time or less energetic employees; I'm sure there are a lot of people who would want to do some work during the week, but not 40 hours, nor the 10 hours of commuting that would entail.

The "make them go back into the workforce" argument needs to deal with the realities of aging and low-level chronic illness, or you end up with Amazon-style painkiller dispensers on the walls of the workplace.

(Note that a lot of the state pension debate is basically the same as the UBI debate. But most of the well-off pensioners you see are on either deferred compensation from more generous times, or savings, or property value)

It’s almost as if we should have a low friction way for people to contract for companies, doing simple non-physical labor, for as many hours a day as they desire.

Something where the investment in the worker is low enough that the company doesn’t need to optimize for someone who will perform at the highest level or have some upward career path over time.

It’s a nice fantasy, but nobody in the US is going to FIRE based on giving Uber rides without being very nearly in a financial position to FIRE without it.

In order to make this happen you have to get rid of age discrimination laws. If you want someone to hire 'less energetic' workers, those employers need to be able to pay them 'less energetic' salaries. That's going to be a tough sell for voters who tend to be in that age block.

It's not necessarily a barrier if you can measure their output - it's not age discrimination if you have a clearly measurable variable that relates to productivity and use it for pay. The old "piecework" model.

It's also not unreasonable or discriminatory to argue that part-time workers can be paid less because they have more overhead .. so long as you apply this across all PT workers.

My company has people who retire at 40 with full pension. To get that though you have to work in some nasty conditions for 20 years. We do our best to make it safe, but there is only so much you can do to make liquid iron safe. I retire at 65 like most people: developing software is not nearly as nasty.

I'm reading Garbage Land at the moment and she mentions that garbage collectors have an incredibly dangerous job, more dangerous than policemen or firemen, for example.

They're risking their lives to do a necessary job, and in that case I see no problem with the early retirement.

It's the traditional number at which to re-evaluate whether you'll need and/or feed someone, innit?

Along those lines, though, I can't help feeling that this result has got to be largely because of the increases in life expectancy rather than falling birth rate (although in some countries the latter is certainly a factor).

I'm Australian and my parents "retired" at 58. They're not quite on cruises and golf days but they're perfectly capable of work even now at 63 if they really wanted. They just don't want. Is it their fault or the governments?

The premise of working for cash is that no-one really wants to do it, which is why you need to give people money in exchange for the work.

So if they don't want to work, and they are entirely self funded, good for them! It's their "fault" and I'm happy for them.

But if they have enough cash flow only because of the current Australian franking credit setup (it no longer merely prevents double taxation, it's a subsidy for investors), tax breaks on Superannuation, and so on, then it's the Government's fault for incorrectly calibrating the benefits in such a way that tax payers end up paying people to be unproductive.

We've also seen low tax rates for most of the rich countries for the last 20/30 years, meaning they could save more and retire earlier, while underfunding pensions and infrastructure for future generations.

It's not just the government's fault, it's short-term thinking by both the government and the voters. Tax rises became anathema in the UK, even for socialist governments like Tony Blair/Gordon Brown.

My parents and other retired people I know feel they've earnt their retirement, when they really haven't. And will be one of the few generations out of the preceding and following to have this sort of luxury of sitting around for a couple of decades doing effectively nothing. Whether it be the rather middle class cruises, golf days, spas, etc. or sitting down the pub or going to bingo or pottering around gardening or sunning it up in Spain or whatever.

They say things like "I worked hard for 35/40 years", I say "So what? The following generations will have to work 50, 55 or even 60 just to pay for the fact you worked 35/40".

At least until automation/robots/AI whatever free humans from work, if it ever happens.

Then again, being in the industry that I am, and most of us are, I will also probably be one of the lucky ones.

> >My parents and other retired people I know feel they've earnt their retirement, when they really haven't.

> Hasn't anyone who can afford to retire earned their retirement? What do you mean by "they really haven't"?

I think what mattmanser is point (if this has to do with state-provided benefits and not strictly employer-provided benefits, though arguments about market performance can be made there) is that, in many cases, these benefits either 1) will not exist at all, 2) exist in a severely reduced form, or 3) will have the goal posts raised periodically (30 years until retirement for you means your children will have to work 50 years until retirement).

If that is a correct interpretation of mattmanser's argument, then he/she is effectively saying that current retirement benefits receivers are receiving their benefits only by encumbering future generations with a greater burden than they bore.

As an aside, this brought to mind the notion that perhaps there is such a thing as time inflation, where past promises don't add up in the future and thus result in moving the goal posts. I've seen this crop up more and more with state pension funds in the United States (which always seem to have assumed the most favorable (and unrealistic) rate of return on their investments).

N.B. My understanding of this stuff is pretty vague, but here's a quick summary of the arguments I've heard on the matter:

I think the grievances might be to do with the amount of money paid into a pension pot versus the size of that pot. At least in the UK, many companies offered generous final-salary pensions, which (as the name suggests) are based on your income and index-linked. These have been basically phased out now, since they're too expensive (i.e. I think they generally cost more to fund than the person originally paid in + any accumulated investment returns). However, for those people who paid into such a scheme, there's no recourse for the scheme providers but to subsidise these expensive pensions with the rest of the communal pot. This means that they necessarily must offer less generous pensions to those who are currently paying in and will draw a pension in future.

I think there are also some arguments in the UK that oil wealth was used for short-term subsidies (e.g. tax cuts), rather than put into a long-term investment fund, like Norway. The people who benefited from that are the people who were alive at the time, and the eventual beneficiaries of their wills.

I don't know how accurate this all is, so would welcome a more informed perspective too.

I'm actually on a final salary scheme but I'm only 33. If I stay in this job for a long time and work for promotions I could end up with a massive sum without even putting anything aside. If I also invest my money into the stock market then I'll be very well off in old age.

One thing about free healthcare and no real property taxes is that its a lot easier to retire early. If they lived in a coastal city in the US they probably couldn't retire because they'd need 40k USD per year in healthcare costs and property taxes.

The government’s primarily, but theirs too because they are the govt., or at least their cohort, friends and neighbours.

The proper thing to do is raise the retirement age to 75, reflecting gains in longevity and economic reality. Other options include some form of part-time mandatory volunteering component to earn the govt. portion of the pension.

However we do it, we are breaking a promise, if you will, that society made to these people when they entered the work force, in that if they endure the indignities and inequities of a salary/wage position for 35 years, then they have earned the freedom to spend the remainder of their time as they see fit.

A promise made by preceding generations that didn't think it through, not by us or people younger than us.

Politicians are now implicitly or explicitly saying that such a promise is clearly not being made to us, why should it be honored as they're the ones who didn't 'pay it forward'?

Right, and that’s exactly what’s happening across the economy. Old programs are being locked, and new entrants are being shunted into modified programs with fewer benefits. We suffer because we know what we’ve lost, but future generations may not know the difference.

The point is most people dont want to work, but society needs people working to provide food, build the things we use, create gas/electricity, help the sick etc. Its an argument about the fairest way to do this.

Allowing some people retire in their fifties while lots of poorer people are looking after them does not seem fair to me at least. (unless perhaps they started working FT at 15)

I do think we should move away from a static age and test the idea that retirement is calculated somewhere between the last 10%-15% of the average life span. And maybe we could do away once and for all with the charade that Social Security is a fund you pay into to receive later on in life and just figure out a better way to distribute X% of annual income taxes to retired folks.

Some unfortunate changes to UK pension laws mean that for some people who hit the - you have to retire or change jobs as you would get massive tax penalties.

One of my friends to early retirement from BT as other wise for his remaining time he would be working for a pittance

Well it is probably the highest number that still fits the threshold for under five. Under five itself is also arbitrary in that it is "show how the demographics have gone older".

{kind=link}

{kind=link}

65 used to be retirement age (for men at least), it clearly needed raising years ago, but was hard to do politically in many countries. It is finally being raised. When pensions were first introduced they were meant to run 5 years, not 20.

In the UK, at least, you could argue we're left paying for a generation of Baby Boomers who are swanning about on cruises, golf days and health spas on pensions they never paid even half towards.

Most are perfectly able to work for another 10 years at least (and if you're younger than 50 you'll have to work those extra 10 years), but for some reason we need economic migrants for economic growth. Even though we're not building anywhere near enough homes, schools, hospitals and transport infrastructure for this mass immigration, and we're not training enough nurses, doctors, teachers. We are effectively just shunting all the economic problems of the end of continual growth 20 years down the line. We even scrapped bursaries for student nurses! Utter madness.

And then, rather ironically, it's this same generation who overwhelmingly voted for Brexit to even further destroy their children's and their children's children prospects because they're not happy about the changing face of the Britain they're not even going to live in.