House values are driven by what people can afford, which is heavily influenced by the interest. If you can afford $1k/mo and 10% of that is interest, 90% is going to principal and you can figure out the math on what your total principal would be. If 20% of that is going to interest, you're still paying $1k, but now your initial principal is much lower, which at scale will drive housing down to some equilibrium where, to be a bit reductive, average people can afford average houses.

My parents bought their house in 1979, for $33k. ~10 years later, when rates had lowered significantly, it was worth $150k.

Not 100% sure about cars, but houses were cheaper. Interest rates being higher means that the monthly payment on a given mortgage amount is higher, meaning the house price that an average buyer can afford goes down. Low interest rates mean that people can afford a more expensive house, and that causes prices to go up.

Anecdotally, my dad complains about paying an interest rate in the teens for the house I grew up in. My parents paid $69K ($188K in 2022 dollars) for the house, which was about a year old. Zillow estimates the same house at $457K today. Obviously not all of the price increase is due to lower interest rates, but the house _was_ much cheaper, so even with a high interest rate, the mortgage was pretty affordable.

Also, returns from other investments tied to interest rates were higher. I seem to recall seeing CD rates >10% in the '80s. I know I had a CD paying >6% as late as the mid '90s. This world where basic banking investments are pointless and pay ~0% is a historic anomaly.

tbh maybe it should stay like that, it's only an anomaly if you start your timeline at the advent of central banking. Interest rates on deposits are a purely mathematical fiction, creating no new value. If people would like to see their old tired moneys sprout new baby moneys out of thin air, they should convert their savings into capital, and effectively invest in productive enterprise. Any capital gain then is by market consensus that new value has been created by your investment in that enterprise.

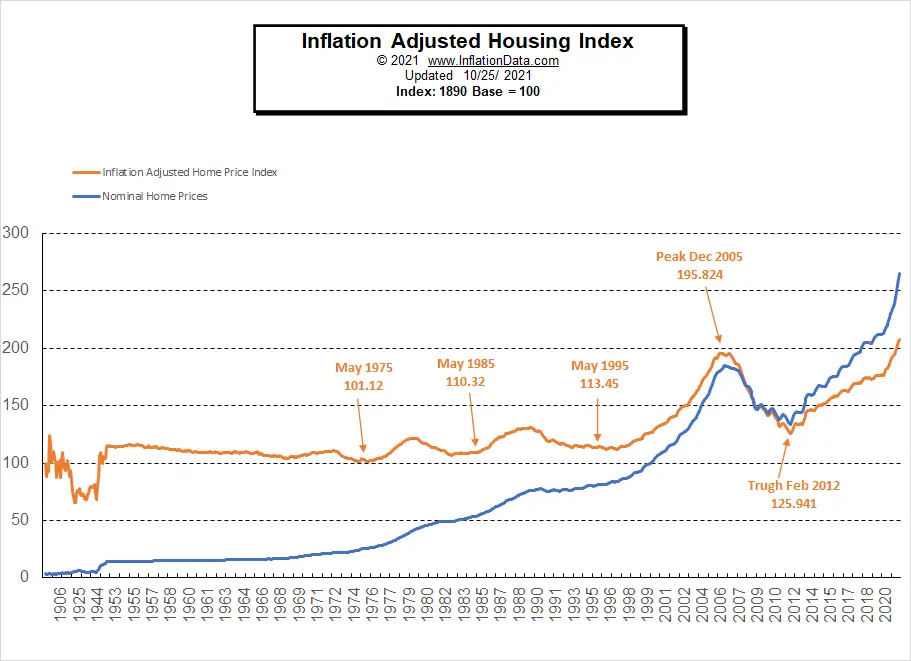

From this chart(https://inflationdata.com/articles/wp-content/uploads/2021/1...) we can see that in inflation adjusted terms, housing was much more affordable prior to about 2001(give or take). I think generally speaking, housing changes hands now much more often than it did before the internet, and there is much more investment/speculation going on as well, which drives a lot of the additional cost nowadays.

I don't think mortgate rates ever broke 20% but were in double-digits.

At that time, though, you needed about 20% down payment to qualify for a mortgage. So you weren't borrowing as much, and houses were smaller and cheaper. It was very difficult for many people to buy a house in those years.

{kind=link}

Fed funds rate in the early 80s were at their historical peak. We are still currently at near historical lows.