Probably not much. The only time the US had a major home price adjustment was 2008 and that was because the housing market was the problem. Currently the housing market is up but not a problem. There aren't crazy foreclosures and there aren't any expected. Tho that can change if we have a big recession absolutely.

Also home prices did not take a very long time to recover all things considered.

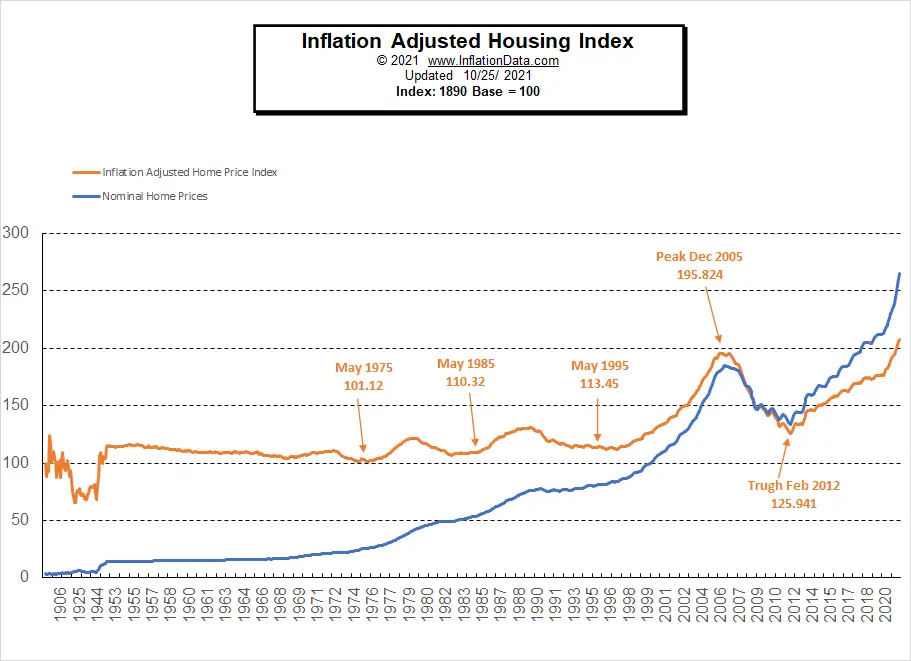

It's always different this time, until it's not. Foreclosure rates aren't high today, but the people who bought extremely expensive houses did so just this year and last. Demand for homes is very high, in large part because hedge funds are buying lots of them... if rates rise, or if prices stabilize, they will pull out, decreasing demand significantly. And will migration to smaller cities/towns continue unabated, (if you haven't moved to Austin/Vegas/Idaho/Montana yet, when do you plan to??) or will that reverse as companies want a physical presence again?

I will agree that last time, the recovery was speedier than anticipated, which only shows that irresponsible economic policy to avoid "economy will crash!!!" is overblown.

> And will migration to smaller cities/towns continue unabated, (if you haven't moved to Austin/Vegas/Idaho/Montana yet, when do you plan to??) or will that reverse as companies want a physical presence again?

Moved to Alaska last year. Not going back to city life - remote forever :)

No. In fact, Alaska doesn't have much net migration, not even the last 2 years. There's quite a lot of churn - people move up here, go through their first Alaskan winter, then move back to the lower 48.

It's not guaranteed and in fact, what you'll likely see is continued home price growth as people pile in the "now or never" mentality as rates increase and mortgages are harder and harder to get a the historic low rates (see Canada).

But in the long run, when mortgage rates go from 3% to 6% affordability goes down - people buy based on monthly payments, not the size of the loan.

Of course if wages drastically increase, the affordability issue could be blunted.

Obviously it is not guaranteed bro. We only have history to base these assumptions on. The history backs the fact that housing prices will not go down - unless there is another major issue like the fraud during 2008, which seems unlikely but not impossible.

Nothing is a guarantee. Silly to base your argument on that. Nothing is for certain.

Everybody “plans” on living in the same house forever. Unfortunately, life gets in the way. Job change, moving for a different school district, divorce, death, etc. Stuff happens.

We'll see. we didn't have inflation like this during the last big downturn in 2008. I also don't think the Fed is going to be able to raise rates as high as they did back in the early 80s.

Because interest rates don't immediately go up. Because the government has ways to ensure that they do not have to pay too much to service the debt. Because the government doesn't have to issue new debt to pay the old debt. Etc.. etc.. etc..

I don't understand these, let's look at them one at a time.

1)

>> Interest rates don't immediately go up.

But the ops question is what if rates did go up (wouldn't it be unaffordable for the government). So your answer seems to be a different scenario to the one discussed? What am I missing?

2)

>> Because the government has ways to ensure that they do not have to pay too much to service the debt.

What ways, specifically? There's just not enough information to be able to make sense of the answer?

3)

>> Because the government doesn't have to issue new debt to pay the old debt.

Can you explain how this works? If they don't issue new debt, where does the money come from the pay the old debt? It's not like they are going to suddenly come into massive surplus by reducing all other spending is it?

4)

>> Etc.. etc.. etc..

I'm seriously thinking about this question, if there's any real reasons, very interested to hear?

I admit I'm not an expert here - but unless someone comes to be with a really good argument why the US Government is on verge of collapse b/c of raising rates (they are the ones why raise rates!!!) I am not sure how much I need to prove the counterpoint?

The inflation in the 2000s was the needle that popped the housing bubble. It wasn't comparable to current levels, but it was high and the Fed tightened aggressively to fight it.

There were a lot of structural problems as well, but rising rates leading to foreclosures set off the chain of events.

{kind=link}